What Is Lex Commissoria? The Forfeiture Clause Explained

What Is Lex Commissoria?

Some legal terms sound ancient because they are. Lex commissoria is a Latin phrase that translates roughly to “forfeiture clause” or “cancellation clause,” and it has been shaping contract law for more than two thousand years. You may not have seen the Latin term in a modern contract, but the idea behind it appears in real estate agreements, loan documents, and commercial leases every day.

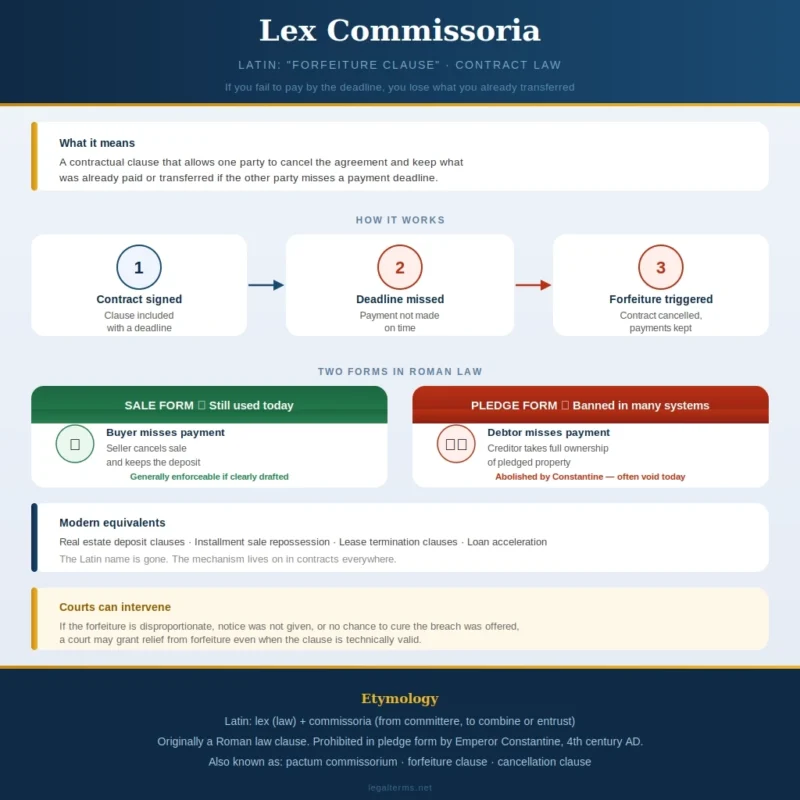

At its core, lex commissoria is a contractual provision that allows one party to cancel an agreement and keep what they have already received if the other party fails to meet a specific obligation, most often a payment, by a fixed deadline. The failure triggers the consequence automatically or by election. There is no need for a court order to start the process. The clause does the work.

That simplicity is both its appeal and the reason courts have sometimes looked at it with suspicion.

Lex Commissoria in Plain English

Picture a buyer who agrees to purchase a piece of land. They pay a deposit and promise to pay the balance by a certain date. The contract includes a clause that says if the full payment is not made on time, the seller may cancel the sale and keep the deposit.

That clause is lex commissoria. The deadline passes. The buyer has not paid. The seller invokes the clause, cancels the sale, and retains the deposit. No lawsuit is needed to reach that outcome. The contract itself provided the remedy in advance.

Now consider the same idea applied to a pledge agreement. A borrower hands over property as security for a loan. The contract says that if the loan is not repaid by a specific date, the lender becomes the outright owner of the pledged property. That is also lex commissoria, though this particular version has a more complicated legal history, as discussed below.

The common thread in both situations is the same: failure to perform by a deadline results in automatic forfeiture of something already transferred or promised.

Origins in Roman Law

Lex commissoria has its roots in classical Roman law, where it operated in two distinct contexts.

In contracts of sale

Roman sellers faced a practical problem. If a buyer agreed to purchase land or other property on credit but later failed to pay, the seller was left in an awkward position, holding the transaction open indefinitely. A lex commissoria clause solved this by giving the seller an option to declare the contract at an end if payment did not arrive on time. The clause was never implied. It always had to be expressly written into the agreement.

Importantly, the clause gave the seller a choice rather than an automatic outcome. The seller could invoke it or waive it, which meant the transaction did not automatically unravel the moment a payment was missed.

In pledge agreements

The second application was more aggressive. A debtor and creditor could agree that if the debt was not repaid by the agreed date, the pledged property would pass outright to the creditor. No sale, no auction, no judicial process. The creditor simply became the owner.

This version proved deeply problematic in practice. Creditors used it to seize property worth far more than the underlying debt, particularly from debtors in desperate circumstances who had little bargaining power. The Roman Emperor Constantine abolished this form of lex commissoria in the fourth century, declaring it unjust and oppressive. The prohibition carried forward into civil law systems across Europe and beyond, and its influence is still visible in modern consumer protection and secured lending legislation.

How It Works in Modern Contracts

The Latin name rarely appears in contemporary contracts, but the underlying mechanism is common. Modern equivalents include:

- Forfeiture clauses in real estate purchase agreements, where a buyer who fails to complete loses their deposit

- Acceleration clauses in loan agreements, where default makes the entire balance immediately due

- Cancellation clauses in installment sale contracts, where missed payments allow the seller to repossess the goods and retain prior payments

- Termination clauses in commercial leases, where a tenant’s breach gives the landlord the right to cancel and re-enter

In each case, the structure is the same as the ancient Roman model: a specific obligation, a deadline or trigger, and a predetermined consequence for failure.

Modern contracts often add procedural requirements that were absent from the original Roman version. A notice period before cancellation, a right to cure the breach within a fixed number of days, and specific written notice requirements are common additions. These reflect the influence of equity and consumer protection principles on what was once a much starker mechanism.

The Two Forms of Lex Commissoria

Understanding lex commissoria fully requires keeping the two original forms distinct, because they are treated very differently in law.

The sale form

When applied to a contract of sale, lex commissoria generally gives the seller the right to rescind the contract and reclaim the property or retain whatever has already been paid. Courts in most jurisdictions will enforce this kind of clause if it is clearly drafted, the deadline was reasonable, and the consequences were agreed to openly by both parties.

The sale form is the less controversial of the two. It functions essentially as a contractually agreed remedy for non-performance, which is something contract law has always recognized.

The pledge form

When applied to a pledge or security arrangement, lex commissoria is treated with far more caution or banned outright in many jurisdictions. The concern is straightforward: allowing a creditor to automatically seize pledged property on default, without any process for valuing the property against the debt, creates obvious potential for abuse.

Many civil law countries, including those in continental Europe and jurisdictions with Roman-Dutch legal heritage, prohibit the pledge form through legislation. The reasoning traces directly back to Constantine’s abolition in Roman law. Even where it is not expressly prohibited, courts often refuse to enforce it as contrary to public policy or as an unconscionable penalty.

Why Courts Look at These Clauses Carefully

Lex commissoria clauses, particularly in their forfeiture form, attract judicial scrutiny for several reasons.

The consequences can be disproportionate. A buyer who has paid most of the purchase price and misses a single deadline may forfeit everything under a strict reading of the clause. Courts in many common law jurisdictions have developed relief from forfeiture as an equitable remedy precisely to address situations where strict enforcement would produce an outcome that shocks the conscience.

The bargaining position of the parties matters. A clause imposed on a consumer or a party with little negotiating power is viewed differently from one negotiated between two sophisticated commercial parties with legal advice. Consumer protection legislation in many countries restricts or modifies the effect of automatic forfeiture provisions in standard-form contracts.

Notice and cure requirements add procedural fairness. Even where a lex commissoria clause is enforceable in principle, courts often require the invoking party to have given reasonable notice of the default and a genuine opportunity to remedy it before the forfeiture takes effect. A clause that purports to operate without any notice at all is more vulnerable to challenge.

Real-World Examples

A property developer sells residential units off-plan. Each contract contains a clause stating that if the buyer fails to pay the balance by the transfer date, the developer may cancel the sale and retain the deposit as liquidated damages. A buyer loses their job, cannot secure financing in time, and misses the deadline. The developer invokes the clause and retains the deposit. Whether the buyer can challenge this depends on the jurisdiction, whether the clause was clearly disclosed, the size of the deposit relative to the purchase price, and whether the developer gave adequate notice.

In a commercial context, a supplier sells equipment to a business under an installment agreement. The contract says that if two consecutive payments are missed, the supplier may repossess the equipment and retain all prior payments as compensation for use and depreciation. The business misses payments during a cash flow crisis. The supplier repossesses. The business challenges the retained payments as a penalty clause. A court will assess whether the amounts retained were a genuine pre-estimate of the supplier’s loss or a disproportionate punishment.

Both examples show the same tension: the party invoking the clause wants certainty and finality. The defaulting party wants proportionality and a second chance. Where courts draw the line between those competing interests varies significantly by jurisdiction and by the specific facts.

Lex Commissoria vs. Related Concepts

Lex commissoria is sometimes confused with neighboring legal concepts. The differences matter.

A liquidated damages clause specifies in advance what compensation will be paid if a party breaches. It focuses on payment of a sum rather than forfeiture of property or cancellation of the contract. Courts apply a similar proportionality analysis to both, but the mechanisms are distinct.

A penalty clause is a provision that imposes a consequence on the breaching party that goes beyond a genuine pre-estimate of the loss. Many jurisdictions refuse to enforce pure penalty clauses, which is why the line between a penalty and a genuine liquidated damages or forfeiture clause is often litigated.

A rescission right allows a party to cancel a contract for breach, but it operates through the general law of contract rather than through a specific agreed clause. Lex commissoria provides the same outcome but through an express contractual mechanism agreed in advance.

Pactum commissorium is sometimes used interchangeably with lex commissoria, particularly in civil law jurisdictions. In some legal systems the two terms describe the same concept. In others, pactum commissorium refers specifically to the pledge form, while lex commissoria is used more broadly. The distinction is terminological rather than substantive in most contexts.

A Few Cautions for Anyone Encountering This Clause

If a contract you are reviewing contains a clause that says the seller may cancel and retain payments on default, or that pledged property will pass to the creditor on non-payment, you are likely looking at a modern version of lex commissoria. The Latin name will rarely appear, but the structure will be recognizable.

The enforceability of such a clause depends on the jurisdiction, the nature of the parties, whether procedural requirements were followed, and whether the consequence is proportionate to the breach. A clause that looks airtight on paper may face equitable challenge in court, particularly if the defaulting party had paid a substantial portion of the price before missing the deadline.

For anyone on the receiving end of such a clause being invoked, the key questions are whether adequate notice was given, whether there was an opportunity to cure the breach, and whether the forfeiture is proportionate. Relief from forfeiture exists in many jurisdictions precisely because the law recognizes that rigid enforcement of these clauses can produce outcomes that no reasonable person would consider just.

Lex commissoria is a mechanism for enforcing contractual discipline. Like most powerful tools in contract law, its legitimacy depends on how it is used.

Frequently Asked Questions

What does lex commissoria mean in simple terms?

Lex commissoria is a clause in a contract that says if one party fails to meet an obligation, usually a payment, by a fixed deadline, the other party can cancel the agreement and keep whatever has already been transferred. It is a forfeiture mechanism built directly into the contract.

Is lex commissoria still used today?

The Latin term rarely appears in modern contracts, but the underlying concept is common. Forfeiture clauses in real estate agreements, repossession provisions in installment sales, and automatic termination clauses in commercial leases all operate on the same principle. The name has changed; the mechanism has not.

Why did Roman law ban part of lex commissoria?

The pledge version of lex commissoria, which allowed creditors to automatically take ownership of pledged property on default, was abolished by Emperor Constantine in the fourth century because it was being used to exploit debtors. Creditors were seizing property worth far more than the underlying debt without any process for accounting for the difference. That prohibition influenced civil law systems across Europe and remains visible in modern consumer lending legislation.

Can a lex commissoria clause be challenged in court?

Yes. Courts in many jurisdictions will examine whether the clause produces a disproportionate result, whether proper notice was given, and whether the defaulting party had a genuine opportunity to cure the breach. Relief from forfeiture is an equitable remedy available in various legal systems precisely to prevent unjust outcomes from the strict enforcement of forfeiture clauses.

What is the difference between lex commissoria and a penalty clause?

A penalty clause imposes a financial payment as a consequence of breach. Lex commissoria operates through forfeiture, meaning the defaulting party loses something already transferred or rights they were entitled to. The distinction matters because courts treat penalty clauses and forfeiture clauses somewhat differently, though both are subject to proportionality scrutiny.

Does lex commissoria apply in common law systems?

Common law jurisdictions do not generally use the term, but forfeiture clauses and automatic termination provisions appear in commercial and real estate contracts throughout common law countries. Courts in those jurisdictions apply their own equitable doctrines, including relief from forfeiture, to control the enforcement of disproportionate clauses. The concept is effectively the same, even if the terminology and the specific legal framework differ.

References

- Cornell Law School – Legal Information Institute (LII): Contracts and Commercial Law

- Black’s Law Dictionary: Definition of Forfeiture, Pledge, and Pactum Commissorium

- LegalTerms.net Editorial Guidelines

- LegalTerms.net Legal Sources and References

LegalTerms.net Editorial Staff produces plain-English explanations of legal terminology for general educational purposes. Content is developed through a structured research process using publicly available legal resources, including statutory frameworks, case law databases, and authoritative legal publications.

All articles are reviewed for clarity, factual consistency, and alignment with widely accepted legal standards before publication. Content does not constitute legal advice.

Learn how our content is created: Content Methodology · Editorial Guidelines · Legal Sources